%20(1).avif)

.avif)

Personal smartphones — and the native calling and messaging apps that run on them — were never designed to meet recordkeeping obligations under SEC Rule 17a-4 or FINRA Rule 4511.

Yet advisors still use iPhone and Android communication apps for client conversations.

Therein lies the risk.

Regulators require complete capture, immutable storage, long-term retention, and supervisory oversight. Native mobile apps provide none of these safeguards.

Which begs the question,

Can native mobile communication apps satisfy SEC compliance requirements on their own?

In this article, we compare the iPlum financial compliance line directly against native mobile calling and messaging apps to determine which solution aligns with SEC and FINRA regulatory standards.

Let’s start by answering the all-important question.

Table of Contents

1. What do the SEC and FINRA actually require from mobile communications?

2. Record capture—automatic vs. user-dependent

3. WORM storage and data integrity

4. Audit readiness and supervision

5. Call recording and FINRA 3170 (taping rule)

6. Personal vs. business communication separation (BYOD risk)

7. Security and data protection

8. iPlum vs. Mobile phone apps for compliance—side-by-Side compliance scorecard

9. Get the iPlum financial line to be SEC and FINRA compliant

What do the SEC and FINRA actually require from mobile communications?

Before we compare iPlum and native mobile communication apps, let’s understand the regulatory baseline first.

SEC and FINRA rules impose specific recordkeeping obligations on business communication conducted through mobile devices. These are

- Complete capture: You must preserve all business-related calls and messages.

- WORM storage: Records must remain non-rewriteable and non-erasable under SEC Rule 17a-4.

- Supervisory access: Compliance officers must review and monitor communications.

- Long-term retention: Records must remain accessible for prescribed retention periods.

- Prompt production: Financial firms must produce records quickly during examinations.

Regulators don’t care what device or app an advisor uses. A desk phone, an iPhone, a texting app, or a third-party messaging platform all count the same.

If an advisor discusses securities business through a native calling app, SMS, iMessage, or another messaging service, those conversations must be saved under SEC and FINRA recordkeeping rules.

And, the advisor cannot argue that the phone allowed deletion. Likewise, a firm cannot argue that the app didn’t provide archiving features. Simply put, technical limits are not an excuse for missing records.

With that out of the way, let’s now compare iPlum vs native mobile phone apps for SEC and FINRA compliance.

Record capture—automatic vs. user-dependent

iPlum far outperforms native mobile phone apps in one area that regulators scrutinize first—automatic record capture.

Let’s unpack that.

Native mobile apps

With native mobile apps, record preservation depends on the advisor.

First, text messages can be deleted. In addition, mobile apps don’t record calls automatically. Sure, you can take screenshots, but these only create partial records. They omit crucial metadata such as timestamps and call duration.

On top of that, third-party recording apps come with operating system and carrier restrictions.

iPlum

The iPlum financial line, in contrast, offers automatic bidirectional call recording. You don’t have to manually activate call recording every time. More importantly, iPlum records inbound and outbound calls based on your firm’s policy.

It also allows you to archive text messages for up to 10 years. That way, your firm maintains a complete communication history for the full regulatory retention period.

WORM storage and data integrity

Record capture doesn’t mean anything if you can’t prove you didn’t change the records. That’s where WORM storage and data integrity come in.

Here’s how iPlum compares to native calling and texting apps on this one.

Native mobile apps

Native messaging apps allow you to edit or delete conversations. In essence, this means you can get rid of an entire communication thread. In addition, you don’t get an immutable archive or a tamper-proof audit trail.

Indeed, some apps offer cloud backups. However, these are not WORM-compliant and are editable.

iPlum

iPlum, unlike native mobile apps. stores communications in WORM-compliant format. With iPlum, records remain non-rewriteable and non-erasable.

And the best part is that the system logs activity and preserves an audit trail tied to each communication. Simply put, iPlum allows you to demonstrate data integrity over the full retention period, something you don’t get with native mobile apps.

Audit readiness and supervision

Preserving records is only half the equation. You also need a communication system that allows you to supervise communication and produce records quickly during an examination.

Let’s compare iPlum and native mobile apps on this one.

Native mobile apps

Supervision is reactive with native mobile apps.

You must inspect each device individually. But more importantly, these apps don’t offer a centralized dashboard where compliance officers can monitor communication activity. In addition, they don’t have a firm-wide searchable archive.

iPlum

iPlum financial compliance line changes this dynamic.

It offers a centralized compliance console with firm-wide visibility. In addition, compliance officers can search, review, and export records by user, date, or number. Meanwhile, iPlum offers up to 10 years of call and text archiving.

Do you know what this means?

If regulators request five years of messages, you can produce them immediately without gathering phones, extracting data, and piecing conversations together manually.

Call recording and FINRA 3170 (taping rule)

Call recording raises a crucial compliance requirement as per the FINRA Rule 3170.

Let’s compare native mobile apps and iPlum here.

Native mobile apps

Native iOS and Android devices restrict automatic call recording.

Therefore, advisors must rely on manual activation or third-party apps. The problem with this setup is that recording may fail or never start.

In addition, native calling apps don’t provide built-in dual-party consent announcements. In all-party consent states, that omission translates to legal exposure.

And, if a firm qualifies as a “taping firm,” inconsistent recording then creates regulatory risk.

iPlum

As stated, iPlum allows you to enforce automatic inbound and outbound call recording based on your firm’s policy.

More specifically, the system plays a built-in consent announcement at the start of recorded calls. On top of that, it catalogs recordings by number and date for supervisory review.

That way, financial firms subject to the taping rule can apply consistent recording standards across all advisors.

Personal vs. business communication separation (BYOD risk)

Mixing personal and business communication creates regulatory exposure, privacy conflicts, and supervisory blind spots.

SEC enforcement around off-channel messaging has made this risk impossible to ignore.

Let’s compare native mobile apps and iPlum on this one.

Native mobile apps

Native calling and messaging apps allow you to combine personal and business conversations in the same thread list.

This means advisors can text clients from personal SMS or iMessage. However, this also implies that firms cannot isolate business communication from private content.

And, during litigation or an SEC inquiry, regulators may demand access to your device, which creates privacy conflicts and reputational risk.

iPlum

iPlum addresses this risk at the architecture level.

The platform provides a dedicated virtual business line on the advisor’s existing device. With iPlum, business calls and messages flow through a separate compliance container under firm policy.

That way, personal conversations remain private. Also, the firm retains administrative control over business communication, including archiving, supervision, and retention.

So, iPlum allows advisors to use one device, but the firm enforces a defensible separation between personal and regulated activity.

Security and data protection

Financial firms must protect regulated communication from unauthorized access, alteration, and internal misuse.

How does iPlum compare to native mobile apps? Let’s find out.

Native mobile apps

Native apps offer control at the user level. They allow advisors to manage device passwords and deletion settings.

As a result, firms cannot enforce uniform password standards across personal devices. In addition, native mobile phone apps don’t offer compliance-grade access logs tied to business communication.

So, if a dispute arises, the firm cannot demonstrate who accessed or altered data.

iPlum

iPlum enforces security at the administrative level.

The platform uses AES-256 encryption for data in transit and at rest. In addition, administrators can implement firm-wide password policies and control access permissions centrally.

The system also logs user activity tied to calls, messages, and account actions. With iPlum, it’s easy for firms to maintain documented oversight of regulated communication.

In addition, they can demonstrate that they implemented consistent security controls during an examination.

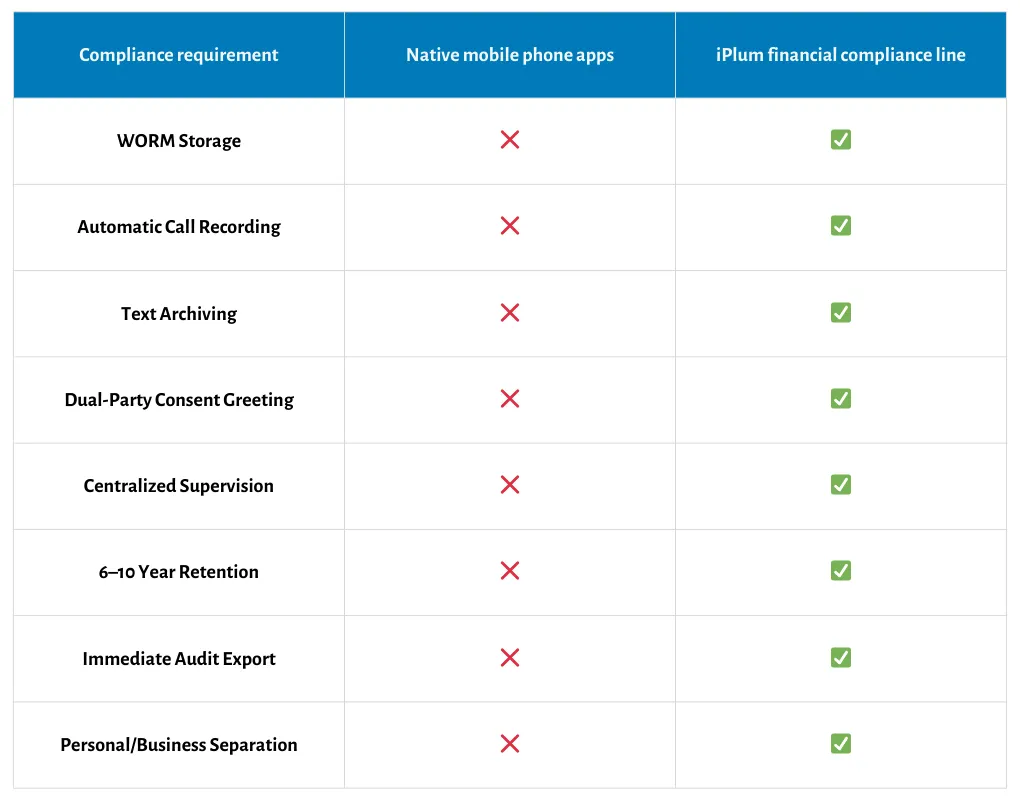

iPlum vs. Mobile phone apps for compliance—side-by-Side compliance scorecard

Before we wrap up, here’s a table summarizing the difference between iPlum and native mobile phone apps for SEC and FINRA compliance.

Get the iPlum financial line to be SEC and FINRA compliant

Native mobile phone apps are convenient. However, they’re not SEC and FINRA compliant.

They allow deletion, restrict automatic recording, lack WORM storage, and offer no centralized supervision. During an examination, those limitations surface quickly.

The iPlum financial compliance line takes a different route.

It enforces automatic call recording, archives text messages for up to 10 years, preserves records in WORM-compliant format, and provides centralized oversight.

As a result, your firm can produce complete, defensible records on demand. It enables you to reduce manual effort, lower legal exposure and operate under policy instead of advisor discretion.

And because SEC enforcement around off-channel communication isn’t slowing down, the safest position is a controlled one.

If your firm conducts business through mobile devices, this is the time to implement the iPlum financial compliance line and move to a defensible compliance posture.

Click the link below to get started.

Sign up for the iPlum financial compliance line.